Straight answers from a licensed New York exterminator and Associate Certified Entomologist (ACE) — serving all five boroughs, in English and Spanish.

Get a Free Estimate →⏱ 7 min read

Quick answer: Before any pest-control vendor works in your building, require three things: a Certificate of Insurance (COI) that names your building and managing agent as Additional Insured, a W-9, and proof of serious liability coverage — in NYC, a $3,000,000 program is a sensible baseline. These protect the building (not the vendor) if something goes wrong, and they signal a real, accountable company. At New York Exterminating, all three are standard — delivered before the first service. Request our COI & W-9 »

If you manage a co-op, condo, or rental building in New York City, the vendors you let through the front door become your risk the moment they start working. A pest-control technician drills into a wall, applies a pesticide in an occupied apartment, or works in a compactor room — and if something goes wrong without the right paperwork in place, the exposure can land on the building, the board, and the managing agent. This guide explains, in plain English, why a pest-control vendor should hand you a COI, a W-9, and proof of strong insurance — what each one actually protects — and how we build all three into our standard operating procedures.

What is a Certificate of Insurance (COI), and why require one?

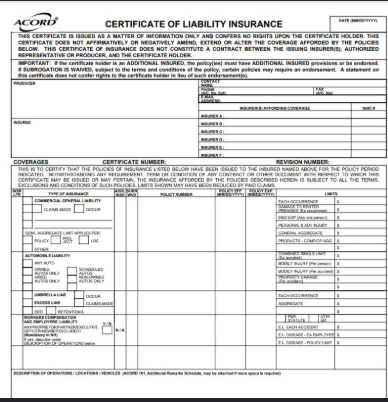

A Certificate of Insurance is a one-page summary (the standard ACORD 25 form) issued by the vendor’s insurance carrier. It proves the vendor actually carries active coverage and shows the limits and policy dates. A vendor saying “we’re insured” means nothing without it — the COI is the proof, straight from the insurer.

When you receive a COI, check for:

- General Liability limits — a common floor is $1,000,000 per occurrence / $2,000,000 aggregate.

- Umbrella / Excess liability — often $2M–$5M, and $5M–$10M+ for high-rise, landmark, or luxury buildings.

- Workers’ Compensation (NYS Form C-105.2) and Disability Benefits (Form DB-120.1) — so an injured technician is covered by the vendor, not your building.

- Additional Insured status for your building and managing agent — on a primary & non-contributory basis, backed by an actual policy endorsement (not just typed on the certificate).

- Current dates — an expired COI protects no one. Reputable vendors track renewals and re-issue automatically.

Why “Additional Insured” is the clause that protects your building

This is the single most important item on the certificate. Additional Insured means your building (and often the managing agent and board) are covered under the vendor’s own policy if the vendor’s work causes injury or property damage. Without it, a claim — a slip in a treated hallway, damage during exclusion work, a resident reaction — can be pushed back onto the building’s policy, raising your premiums or exceeding your coverage. “Primary & non-contributory” language means the vendor’s policy pays first, before yours is ever touched. Requiring it is one of the simplest ways a board protects its shareholders.

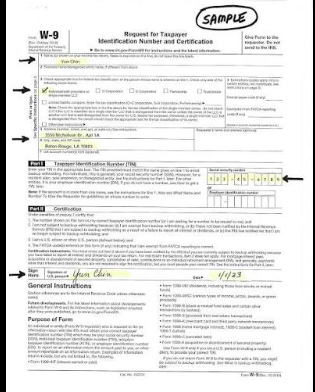

What is a W-9, and why require it?

A W-9 is the IRS form that captures a vendor’s legal business name, entity type, and Taxpayer Identification Number (EIN). You require it for two reasons. First, tax compliance: it lets your management company issue an accurate 1099 and keeps the building’s books clean for audits. Second, legitimacy: a vendor who can immediately produce a W-9 is a real, registered business — not an unlicensed handyman taking cash, which (for pest work) is a compliance problem in its own right under NYC’s building pest laws.

Why $3,000,000 in coverage matters in New York City

NYC raises the stakes. Buildings are high-value, densely occupied, and often luxury or landmarked; pesticide application happens inside people’s homes; and a single serious incident can blow past a $1,000,000 limit quickly once medical, legal, and property costs stack up. That is why many managing agents and boards require an umbrella into the $5M–$10M range for larger properties, and why a $3,000,000 liability program is a sensible baseline for serious building work. For a board, carrying — and verifying — adequate vendor coverage is part of its fiduciary duty to owners and shareholders. Under-insuring the vendor quietly transfers risk to the building.

How New York Exterminating builds this into our SOPs

We don’t treat insurance and paperwork as an afterthought — it’s part of how we onboard every building, before the first service:

- We carry $3,000,000 in liability coverage (general liability + umbrella).

- We issue a COI naming your building and managing agent as Additional Insured, primary & non-contributory, with endorsements — not just a name typed on the form.

- Our W-9 is ready on request, along with our NYSDEC pest-control license, workers’ comp (C-105.2), and disability (DB-120.1).

- Every document is kept current and delivered through your 24/7 customer portal, alongside service work orders, pesticide labels, and reports.

- We’re set up for the vendor-credentialing platforms managing agents use, so onboarding is fast.

In other words, the documents your approval process needs are already prepared. See exactly how this fits into a full building pest-control program, or read why a vendor’s license and credentials matter just as much as its insurance.

Red flags: what an uninsured or under-insured vendor exposes you to

- No COI, or “we’ll send it later.” If it isn’t in hand before work starts, assume it doesn’t exist.

- A COI with no Additional Insured endorsement. Your building isn’t actually protected.

- An expired certificate. Coverage may have lapsed entirely.

- No workers’ compensation. If an uninsured technician is hurt on your property, the building can be drawn into the claim.

- Cash-only / unlicensed “handyman” pest work. Beyond the insurance gap, it can violate NYC pest-control and Local Law 55 requirements.

- No W-9. A legitimate business can produce one in minutes.

The bottom line for boards and managing agents

Requiring a COI, a W-9, and strong insurance isn’t bureaucracy — it’s risk management. It keeps liability where it belongs (on the vendor), keeps your building’s books and compliance clean, and filters out operators who cut corners. The best vendors welcome the request, because they already have everything ready. If you’d like ours, we’ll send it the same day.

Related resources

Property-management pest control programs · Commercial pest control · Co-op & condo boards · NYC pest-control laws & building compliance · Protect your DOH letter grade · Pest control cost in NYC · Why your exterminator’s license matters · Meet Jorge Bedoya, ACE

A Brooklyn-based, NYSDEC-registered company (Reg. #15140) led by Jorge Bedoya, an Associate Certified Entomologist (ACE). For pests in your home or building, NYE provides IPM-based, low-exposure control matched to the exact pest and verified with a follow-up. ACE-led work comes with a client portal of service reports and photos, fully bilingual service, and no long-term contract.

Pest-Vendor Insurance FAQ

What insurance should a NYC pest-control company carry?

At minimum, general liability (commonly $1M per occurrence / $2M aggregate), workers’ compensation, and disability benefits. For building work in NYC, an umbrella that brings total coverage into the $3M–$10M range is a sensible baseline, with higher limits for high-rise, landmark, or luxury properties.

What does “Additional Insured” mean and why does it matter?

It means your building and managing agent are covered under the vendor’s policy if the vendor’s work causes injury or damage. “Primary & non-contributory” means the vendor’s policy pays first, before your building’s. Without this endorsement, claims can fall back on the building.

Why do I need a W-9 from my pest vendor?

It confirms the vendor is a registered business with a valid tax ID, lets your management company issue an accurate 1099, and keeps the building’s records clean for audits.

Is $1,000,000 enough coverage?

It’s a common floor, but in NYC a single serious claim can exceed it. Many boards and agents require an umbrella into the $5M–$10M range; a $3M program is a reasonable baseline for serious building work.

How fast can New York Exterminating provide a COI?

Typically the same day. Just tell us the exact legal names to list as Additional Insured (building entity and managing agent) and we’ll have our carrier issue it.

Do you name both the building and the managing agent?

Yes — we routinely name the building entity and the managing agent (and the board where requested) as Additional Insured, primary & non-contributory.